Insurance. The word itself evokes different reactions. The range of emotions expands when we mention life insurance. And if we add the word trust–life insurance trust–clients may stop listening altogether. But now is exactly the time to be thinking of planning with an irrevocable life insurance trust.

Life insurance is a cornerstone of risk management and business succession, tax, wealth, and estate planning. Its place in clients’ overall planning varies. Life insurance may provide simple income replacement for a growing family dependent upon the earning capacity of an early-career parent. Or it may be the source of funding a buy-sell agreement for a business enterprise. Insurance is also a resource for liquidity to fund anticipated estate tax liability and is used in charitable gift planning. Knowledgeable insurance professionals provide valuable guidance on the type of insurance to meet a client’s goals while tax and legal advisors provide advice on how to own and transfer the benefit of insurance to meet client goals with minimal tax burdens.

This article discusses the types of life insurance, the purposes of life insurance in a client’s wealth and estate plan, the income tax and creditor protection associated with life insurance, and the design and administration of irrevocable insurance trusts to own and administer life insurance, all of which is of growing relevance in the current environment of increasing income tax rates, decreasing estate tax exclusions, and potential changes in the taxation of appreciated assets at death. Additional advanced split-dollar life insurance planning is also discussed.

Protect and Preserve Wealth

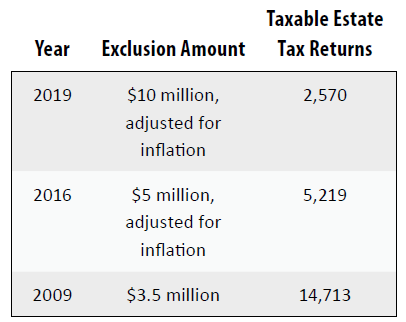

As the tide of increasing estate tax exclusion levels turns (which we expect it to do by 2022) more estates will become taxable. In 2019 (the last year for which data is available) when the estate tax exclusion was $10 million, adjusted for inflation, the IRS reported 2,570 taxable estate tax returns filed. This is more than twice the number of estate tax returns filed in 2016, the final year of the $5 million, adjusted for inflation, exclusion amount. In 2009, 14,713 taxable returns were filed under the $3.5 million exclusion amount (up from $2 million in 2008). Whether the current $11.7 million exclusion reverts to $5 million adjusted for inflation, $3.5 million not adjusted for inflation, or some other lower-than-current level, more estates will owe estate tax. Life insurance is a source of liquidity in taxable estates. Life insurance held in a well-designed and administered irrevocable life insurance trust can be excluded from the taxable estate and provide overall liquidity to the family balance sheet.

Leverage Planning

In the midst of the flurry of tax proposals, we have yet to see a proposal that would do away with the annual gift exclusion ($15,000 in 2021) in its entirety. The annual exclusion has been part of the Internal Revenue Code (Code) for decades and we expect it to remain, although some of the details may change. Leveraging the annual gift tax exclusion will become more important as the lifetime exclusion decreases. The annual gift tax exclusion, applied to cover annual premium payments in an irrevocable life insurance trust, is an effective means of leverage, so long as the total premiums paid do not exceed the benefits paid on the policy.

Simplicity

Do we really mean simplicity? Yes, in a sense. In order for an irrevocable insurance trust to work to remove assets from the insured’s estate, attention needs to be paid to the administration of the trust during the insured’s lifetime. This work of the trustee comes with associated duties and liabilities. In Illinois and certain other states, state law has been modernized to simplify a trustee’s investment duties and minimize the associated liabilities of a trustee during the time the policy is held in trust and the insured settlor of the trust is still living. In Illinois, for example, during the settlor insured’s lifetime, the trustee may hold an insurance policy in trust: (i) without determining that the policy is a proper investment for the trust; (ii) without diversifying the investments of the trust; and (iii) without monitoring the financial and physical condition of the insured. These are important considerations for both individual and professional trustees given the unique attributes of life insurance as an asset of an irrevocable trust.

CLICK HERE to read the full article, which was originally published in ALI CLE’s The Practical Tax Lawyer.